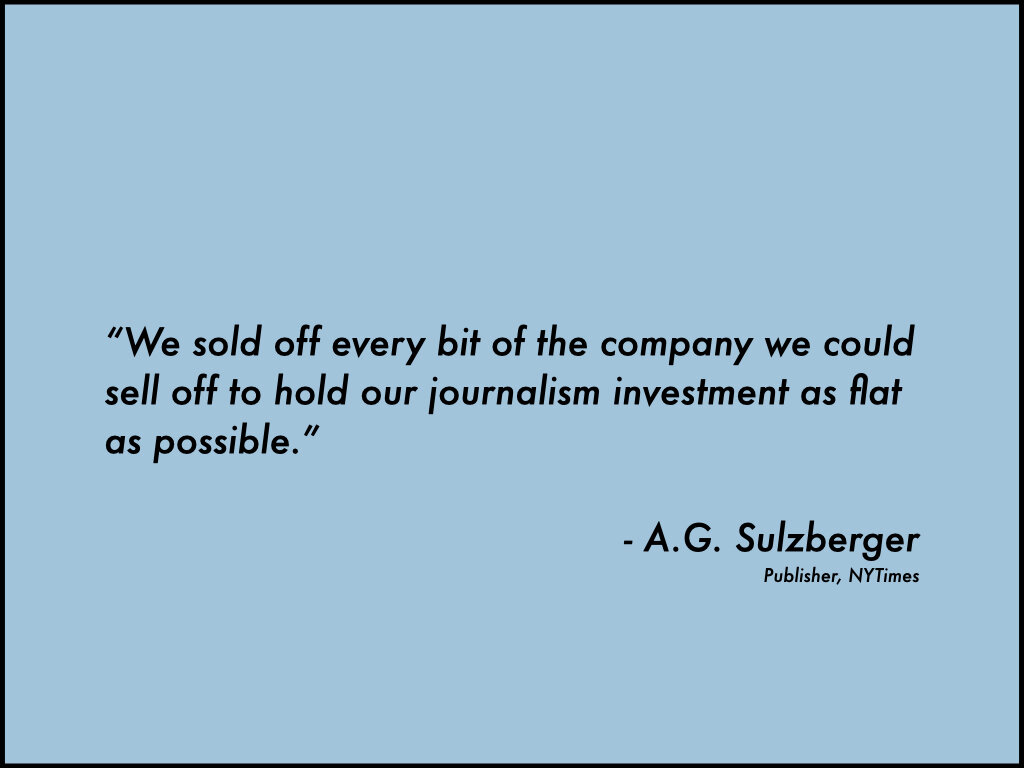

CLICK TO EXPAND

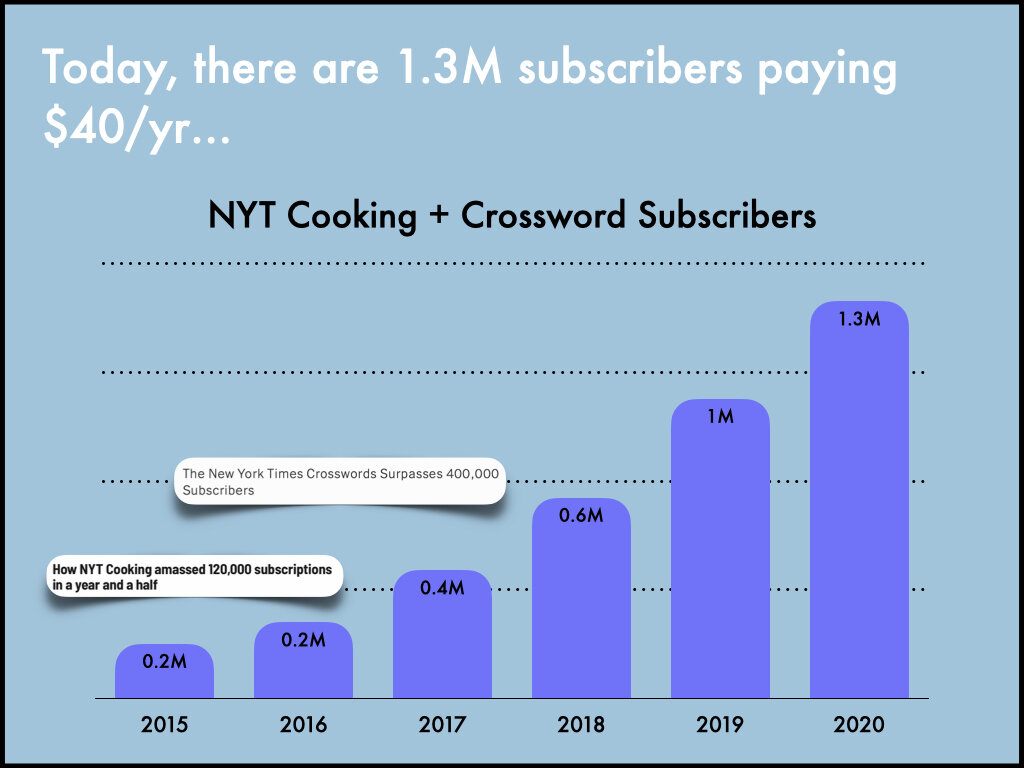

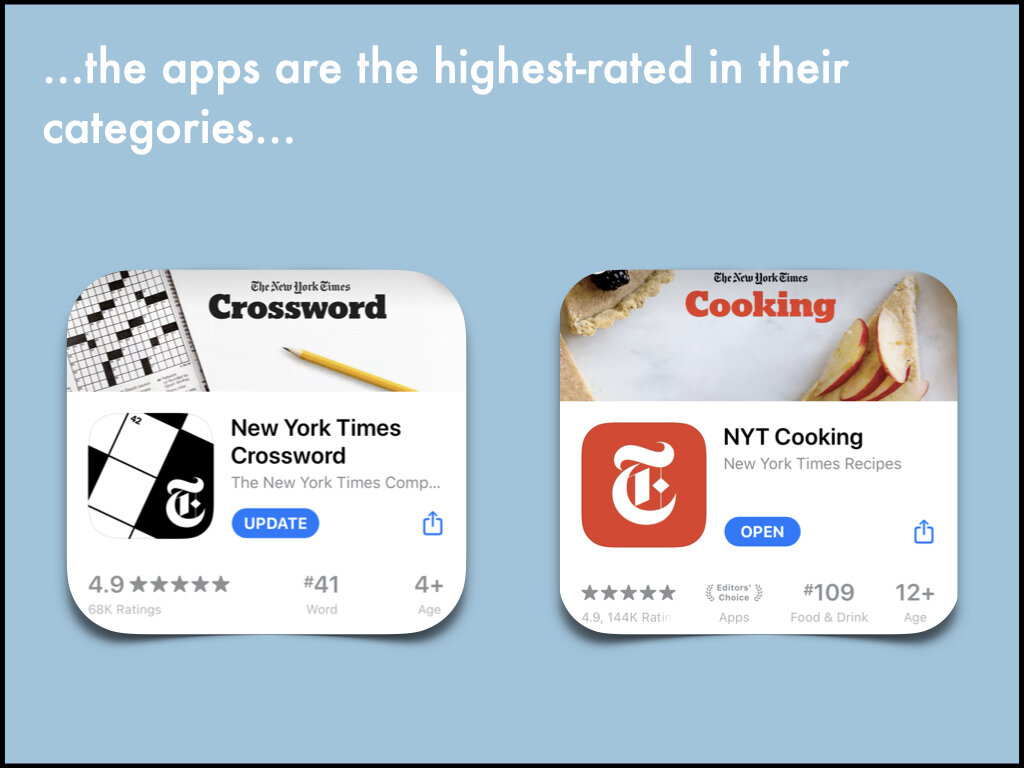

The (Not Failing) New York Times

in Companies

CLICK TO EXPAND

WHAT VISA DOES

Visa sits at the center of more than half of the world's credit card transactions, connecting cardholders (and their banks) on one side, with merchants (and their banks) on the other. Because there are thousands of banks, millions of merchants, and billions of consumers, it would be far too complex for every entity to have a direct relationship with every other entity. So Visa acts as a centralized operator, developing technology, maintaining infrastructure, and setting operating standards for all parties.

Consider a small merchant bank in Thailand that wants to enable their clients (i.e., merchants) to accept credit cards from tourists. For a transaction to take place, the Thai bank must have a way of communicating with each tourist’s bank so that the transaction can be approved, and money can be transferred. That means developing software that integrates with every single one of the tourist banks, and every single one of the merchant point of sale systems. There has to be support for hundreds of languages and currencies, all while ensuring compliance with thousands of local laws and regulations. Operating standards must be established so that the banks can settle merchandise returns, cardholder disputes, and fraudulent transactions. And the entire process has to be automatic, real-time, and operate with zero failure or downtime. The truth is, most banks simply don't have the resources to do this with more than a few other banks—let alone thousands. So Visa does it for them.

Visa's value proposition is simple: integrate with us, and gain instant access to a network of 3 billion cards, 16,000 banks, and 44 million merchants in 200+ countries and territories.

HOW VISA MAKES MONEY

The beauty of Visa's business model is that they get paid every time one of their cards are used—a flat fee of $.07, plus 0.11% of the transaction amount (and more for international transactions). So the more dollars that flow through Visa’s network, and the more transactions that they process, the more money they make.

Visa makes money three ways: service fees, data processing fees, and—if the transaction involves banks in two different countries—cross-border fees.

1. SERVICE FEES - To participate in the Visa network (i.e., accept/issue Visa cards), banks pay Visa a small percentage of the total dollar amount of every transaction. So the more a product costs, the more money Visa makes. That makes payment volume—which is the total dollar amount spent on Visa’s network—the primary driver of this revenue source. What's great about this type of revenue is that it's a built-in hedge against inflation; if the cost of goods rises, Visa's revenue automatically rises with it.

In 2018, Visa’s services revenue was $8.9 billion on $8.1 trillion of network spend. That means Visa pockets about 0.11% of every transaction, which is known as the service fee yield.

2. DATA PROCESSING FEES - Visa also earns a fixed/flat fee per transaction for settling transactions and transferring funds between banks. These revenues are based on the total number of transactions made on Visa's network, regardless of the dollar amount. What’s great about this type of revenue is that it costs Visa about the same to process one million transactions as it does one hundred billion; so each incremental transaction is close to 100% profit.

In 2018, Visa’s data processing revenue was $9 billion, on 124 billion transactions. That works out to $0.07 per transaction.

3. CROSS-BORDER FEES - Visa earns additional revenue for processing cross-border transactions; that is, when the merchant's bank and cardholder's bank are in different countries. Because these types of transactions are more complex, require currency conversion, and tend to have a higher rate of fraud, the fees are much higher than those on domestic transactions. The primary driver of this revenue source is the total cross-border dollar amount; however, Visa does not break this number out.

In 2018, Visa’s cross-border revenue was $7.2 billion. The yield is estimated to be around 1%, making it Visa’s highest-yielding and most profitable product—by far.

WHAT MAKES VISA SPECIAL

VISA’S BUSINESS IS A VIRTUOUS CYCLE. As more cardholders spend more money on their Visa cards, more merchants will accept Visa in order to capture those sales. And as the number of merchants who accept Visa grows, consumers are more likely to use it. That translates into an ever-growing amount of dollars and transactions flowing over Visa’s network; and thus, an ever-growing stream of service, data processing, and cross-border revenue.

HIGH OPERATING LEVERAGE. Visa's business is all about scale. That's because the company's fixed costs are high, but the cost of processing a transaction is essentially zero. Said more simply, it takes a big upfront investment in computers, servers, personnel, marketing, and legal fees to run Visa. But those costs don't increase as volume increases; i.e., they're “fixed”. So as Visa processes more transactions through their network, profit swells. As a result, the company’s operating margin has increased from 40% to 65%:

And the total expense per transaction has dropped from a dime to a nickel; of which only half of a penny goes to the processing cost. Both trends are likely to continue.

NEW ENTRANTS RELY ON VISA. (and Mastercard) A few years ago, many predicted the payment industry would soon be “disrupted” to the detriment of Visa (and Mastercard). They were half right. Companies like Apple, Google, Amazon, Stripe, Square, PayPal (and PayPal-owned Venmo) did invent novel new ways to make and process payments. But rather than compete head-to-head with Visa and Mastercard, these companies chose to partner instead. Why? Because any would-be competitor would have to invest billions of dollars in networking infrastructure so that transactions can be processed in real-time and with practically zero failures. They would need to establish relationships—one by one—with 16,000 banks worldwide. They’d need to write complex software that works with each of those banks, as well as millions of payment terminals. And they would need to ensure compliance with thousands of financial laws and regulations from over 200 countries. Or they could just partner with Visa.

DOESN’T NEED CAPITAL TO GROW. Since 2010, Visa’s revenue, earnings, and cash flows have grown 11%, 17%, and 22% per year, respectively. What’s remarkable about this growth is that it has been achieved with minimal investment—equity has only increased by about 4% per year, and CapEx (as a percent of revenue) has been flat. So what has Visa done with all that excess cash? They’ve returned it to shareholders. Of the $51 billion Visa has earned since 2010, $49 billion has been paid to shareholders in the form of buybacks and dividends.

HOW VISA CAN KEEP GROWING

After growing payment and transaction volume 10%+ per year (and FCF/S 20%+) for over a decade, it’s hard to imagine Visa has much growth left. But the company is likely to sustain—or even accelerate—their already-high growth rate thanks to five tailwinds:

1. INCREASE IN WORLDWIDE ECONOMIC GROWTH & INFLATION. Visa’s fees are like a royalty on economic growth and spend. So as the economy grows, so does Visa. For most businesses, the downside to economic growth is inflation, which means higher input costs. If the company can’t pass on price increases to its customers, volume (and profitability) shrink. Visa doesn’t have this problem. That’s because they earn a percentage of every transaction—so as things become more expensive, Visa makes more money.

2. CONVERSION OF CASH/CHECK TO CARD/ELECTRONIC. Consumers increasingly prefer using credit cards, debit cards, and electronic forms of payment over cash and check. That’s good news for Visa, since the less cash is used, the more money they make. But even as digital forms of payment have begun to supplant cash, there is still a long way to go. 80% of worldwide transactions and 42% of payment volume (i.e., total dollar spend) are still done in cash. By Visa’s estimate, $17 trillion is still spent on cash and check each year. That’s a big opportunity.

3. GROWTH OF E-COMMERCE. E-commerce spend is growing at 4x the rate of physical retail. This is more good news for Visa because the company captures $0.43 of every dollar spent online versus $0.15 for physical. The reason is simple—you can’t use cash online. So the more purchasing that moves online, the more Visa benefits.

But even though e-commerce has been growing 20% per year (versus 5% for physical retail), there is still a long way to go. Today, only around 13% ($3.4 trillion) of total retail sales occur online, providing Visa another long runway for growth.

4. NEW MARKET SEGMENTS. Visa’s primary segment has always been consumer-to-business (i.e., C2B). But Visa is expanding into new segments (e.g., B2B, P2P, G2C, C2G) where payments have traditionally not been electronic. For example: payments from businesses to suppliers (i.e., B2B) often rely on checks, bank transfers, and invoicing; sending money to a friend (i.e., P2P) is usually done with cash or check; and when governments need to disburse money to citizens (i.e., G2C) for things like disaster relief, medical subsidies, and tax refunds, check or wire transfers are used. Visa believes $30 trillion is spent in these segments, so if they are successful in converting even a tiny fraction of it, it would be a huge boon for the company.

5. VISA EUROPE PRICE INCREASES. In 2016, Visa acquired Visa Europe for $23 billion. Though the two companies shared branding, research, and some operational resources, Visa Europe was a separate company that was collectively owned by its member banks. That meant it wasn’t run as a for-profit business. But it will be now that Visa owns it.

The acquisition of Visa Europe explains the recent dip in the service fee yield and the data processing fee per transaction. Before the acquisition, Visa's data processing fee per transaction was $.078; following it, it dropped to $.07. And service fee yield—that is the percent of total payment volume that Visa keeps—dropped from 0.13% to 0.11%. If Visa can bring Visa Europe pricing on par with the rest of the company—as is expected—service revenues would increase by about $1.6 billion, and data processing revenues would increase by $900 million. Both would flow straight to operating income.

Here’s what it looks like when we add it all up: 2 - 4% for natural economic growth and inflation; a $17 trillion opportunity for converting cash and check; $3.5 billion annual e-commerce spend (which is growing 20%/yr); a $30 trillion opportunity in new payment segments; and an increase to service fee yield and per transaction data processing fees.

With so many tailwinds, it would not be surprising for Visa's payment and transaction volume to continue growing around 10% per year.

CONCLUSION

Visa is a great business. The company has, in effect, a royalty on global economic expansion and consumption. Would-be competitors have chosen to partner with Visa rather than compete head-to-head. And Visa is poised to keep growing double digits thanks to several tailwinds, like the digitization of money, the growth of e-commerce, new market segments, and Visa Europe price increases. And because the business requires very little capital and benefits from high operating leverage, all growth should fall straight to the bottom line.

These are the hallmarks of one of the best businesses on the planet. What that business is worth comes down to assumptions made about payment and transaction volume growth, yields/processing fees, the sustainability of the company’s competitive position, and long-term operating margins.

You can model those assumptions here:

INTRODUCTION

Visa is one of the biggest companies in the world. Cards bearing the Visa logo are used more than 340 million times every day. And the Visa brand is one of the most-recognized on the planet. Yet unlike other companies of similar size and ubiquity, few people know what Visa does, how they make money, or why they even exist.

To understand, it helps to look at the company’s history.

BANKS

"A bank is the place for a poor man to put his money so that a rich man can get it when he wants."

At the turn of the century, most Americans found it difficult to borrow money from banks. For a time, this wasn't a big deal. Not when most Americans lived with a set of low-cost goods, largely unchanged for centuries: furniture, clothing, crude farm tools, basic kitchen and household items, perhaps a wagon. But toward the end of the 19th century, the old way of doing things was challenged by new, technologically advanced goods that flooded the American market. These new goods—cars, telephones, sewing machines, refrigerators—had obvious advantages. They enabled people to do more, in less time, and with less effort than previously possible.

There was just one problem: most people couldn't afford them.

INSTALLMENT CREDIT

Merchants and manufacturers came up with a solution: installment credit.

For consumers who needed a car, a new set of tools, or a dishwasher—but couldn't afford to pay for it outright—installment credit allowed them to put a little money down, and pay off the remaining debt in small monthly increments. Goods that would've taken years to save for could now be had for a few dollars a month. Almost overnight, the unaffordable became affordable.

It wasn't just consumers who benefited. Merchants were quick to realize that people are far more likely to buy something when they can pay for it later. So for any retailer or manufacturer looking to increase sales, selling on installment credit was a simple and effective way to do it. The plans were so popular that by 1930, most durable goods—including 65% of cars; 85% of furniture; 75% of washing machines; 65% of vacuum cleaners; 20% of jewelry; and 75% of radio sets—were sold on credit.

But lending money was not without cost: merchants had to asses each individual customer's creditworthiness; bear the risk of late or nonpayment; and shoulder all of the back office headaches and expenses that came with managing thousands of individual accounts—like billing/collection, postage, stationery, and customer service reps. It was cumbersome for customers, too. Every time they wanted to make a purchase on credit, they had to shlep to the merchant, sit down with an associate, hand over their financial and employment history, and fill out stacks of paperwork.

The process was a pain—and it was why banks avoided making small loans in the first place. That is, except for one bank.

BANK OF AMERICA…

By the 1950s, Bank of America had grown into the largest bank in the country—and it did so by being the one big bank willing to lend to middle-class consumers. “We were always a leader in installment credit. Anything you could buy on time, we financed: student loans, cars, boats, trailers, home loans, personal loans, you name it", recalls Ken Larkin, a lifelong Bank of America executive. “People would come into the bank 4-5 times a year, whenever they needed extra funds. There was vacation. There were back-to-school clothes. There were the holidays. There was tax time. There were medical emergencies."

Though the bank flourished because of its willingness to lend money to the middle class, it still suffered the same pains as merchants who sold on installment plans: the reams of paperwork; the tens of thousands of salaried loan officers; the record-keeping; the millions of accounts. Bank of America wanted to make this process more efficient—and thus, more profitable. To do that, they turned to the credit card.

…DINER’S CLUB…

The idea of a credit card was not new. Diner's Club was the first to popularize the concept in 1951, with a general-purpose card that could be used at multiple merchants. The card differed from other available forms of credit in an important way: instead of receiving credit directly from a merchant, customers received a card—and its associated credit—from a third-party organization not owned by the merchant itself. That third party was Diner's Club.

Diner's Club signed up different merchants to accept their card, and promised to reimburse them for any charges made on it—even if the cardholder never paid their bill. Thus, the merchant received all of the benefits of selling on credit, without any of the headaches (e.g., bookkeeping, billing, and collecting). And customers benefitted too. For the first time, they could use a single card to make purchases at many merchants. Within 12 months, the card had 42,000 members and was accepted by 330 merchants.

…BANK OF AMERICA

The success of Diner's Club put banks on notice. So in 1958, Bank of America decided to launch their own card—but with a twist. Unlike Diner's Club, Bank of America's card wouldn't require customers to settle their bill in full each month. Rather, their card would offer revolving credit, which differed from installment credit in that there was no fixed number of payments. So borrowers could draw as much as they like, whenever they like, for whatever purchase they like. All without ever setting foot in a bank.

Bank of America viewed their credit card as a way to provide customers with an instant, no-questions-asked personal loan. Their hope was that by giving customers greater control, the bank could cut down on the time and money spent on processing loans.

“It handed the keys to the customers. It was he or she alone who got to make the decisions about how, and when, to spend large sums of money—and how, and when, to pay the money back. It could be used impulsively or carefully; frequently or sparingly; for emergencies or for shopping sprees. And then, when the bill arrived, it was he or she alone who decided whether to pay back the money all at once (with no interest), or in installments (with interest). The crucial point is that the customer was in control of financial decisions that had always before required the explicit approval of a banker or merchant. One major reason previous credit card programs had flopped was that most banks feared giving their customers that much control. Bank of America had no such qualms.” [1]

The next step was getting people to use the card. And merchants to accept it.

BANKAMERICARD

"A successful credit card program requires the participation of not just customers but store owners as well. In fact, it requires thousands of store owners, all of whom have to be recruited with the promise that there will be enough cardholders to make accepting the card—and handing over a percent of the purchase price to a bank—worth their while. At the same time the bank is recruiting merchants, though, it must also recruit cardholders—promising them that there will be enough merchants signed up to make carrying the card worth their while. It's a chicken-or-egg dilemma. What comes first, the customers or the merchants?" [1]

Bank of America's solution to this problem was The Fresno Drop. The bank decided that rather than try to sign up new customers, they would pre-approve existing Bank of America customers living in Fresno, CA. Why Fresno? Because 45% of the city's families were Bank of America customers; and because if it flopped, Fresno's relative isolation would limit the damage to the bank's reputation. With so many of the city's residents set to become cardholders practically overnight, merchants had no choice but to take notice. And so they began to sign on.

"It was the smaller merchants who first came around. Larkin remembers visiting a drugstore, hoping to persuade its owner to accept BankAmericard. "When I explained the concept of our credit card," he says, "the man almost knelt down and kissed my feet. 'You'll be the savior of my business,' he said. We went into his back office," Larkin continues. "He had three girls working on bookkeeping machines, each handling ~ 1,500 accounts. I looked at the size of the accounts: $4.58; $12.82. And he was sending out monthly bills on these accounts. Then the customers paid him maybe three or four months later. Think of what this man was spending on postage, labor, envelopes, stationery! His accounts receivables were dragging him under." [1]

On September 18, 1958, sixty thousand unwitting Fresno residents opened their mailboxes to find the first true credit card: the “BankAmericard”. Within a year the card was expanded to Los Angeles, San Francisco, Sacramento, Bakersfield, and Modesto. It was a disaster. Fraud was rampant. 22% of cardholders were late on payment. Large merchants were resistant to the idea of paying a percentage of each sale to Bank of America. After 15 months, the program lost $20m (about $170m today).

Other banks, seeing the early losses of Bank of America's program, stayed away. But this was fortuitous—because by the time Bank of America turned their program profitable three years later, it was too late for competitors to catch up. The BankAmericard had already blanketed the entire state of California. And then the virtuous cycle began: year after year, more cardholders were spending more money on their BankAmericards. To capture those sales, more merchants began to participate in the program. And the more merchants that accepted the card, the more customers used it. It was a cycle that rival banks would be hard pressed to replicate. After all, what customer is going to use a card that isn't accepted by most merchants; and what merchant is going to accept a card that no one uses?

FRANCHISE

By the mid-1960s, the BankAmericard program had overcome its initial difficulties and was generating solid profits. But because Depression-era bank laws forbade banks from having out-of-state customers, the BankAmericard could only be used in California. So in 1966, to grow the card program beyond their home state, Bank of America decided to franchise the BankAmericard to select banks all over the world. Under the program, Bank of America charged each licensee bank a $25,000 entry fee, plus a royalty of ~0.5% on total cardholder spend. In return, Bank of America would show the smaller bank how to run a credit card operation.

Merchants that were signed up by the licensee banks agreed to accept all BankAmericards, allowing consumers to use their BankAmericards at any participating merchant worldwide—regardless of which bank the merchant used. In short, the program enabled merchants and customers to have different banks for the first time.

This was a big deal because now a customer from Albany could get a BankAmericard from their local bank; and they could use that card to buy something from a merchant affiliated with a bank in Hawaii. It looked like a win-win: merchants exponentially expanded their pool of available customers, and customers got to use their card at a growing number of merchants.

AUTHORIZATION & INTERCHANGE

But almost as soon as it launched, the licensing program began to fall apart.

The first problem was authorization. Authorization is what makes it possible for a merchant to know that a customer's card is valid (i.e., not stolen), and that he isn't exceeding his credit limit. Authorizing a transaction is relatively easy when the merchant and customer belong to the same bank: the merchant simply calls their bank to see if the customer's account is in good standing, and the bank looks up the cardholder's account. But with the franchise system, the customer and merchant often had different banks. This made authorizing a transaction much more complicated.

"The merchant had to call his bank, who then put the merchant on hold while they called the cardholder's bank. The cardholder's bank then put the merchant's bank on hold while they pulled out a big printout to look up the customer's balance to see if the purchase could be approved—all while the customer and merchant stood there in the store, waiting for the reply. And that was when the system was operating smoothly. Sometimes the merchant got a busy signal. Other times his calls went unanswered, something that happened most often when a customer with a card from an East Coast bank tried to buy something late in the day in California. And if the merchant couldn't get through, they then had to decide whether to accept the card or lose the sale. And if the merchant took the card, and it turned out to be stolen, all hell would break loose as the banks fought over who should absorb the losses." [1]

The second problem was the behind-the-scenes system—designed to facilitate transactions between banks—known as interchange.

"It is impossible to overstate the importance of a workable interchange system; without it, nationwide credit cards simply cannot exist. Because the vast majority of credit card transactions involve two separate banks—one that handles the merchant's business, and another that issues the credit card to the customer—banks have to have a way that allows them to “settle” their accounts with each other." [1]

When a Bank of New York cardholder bought something at a merchant who was affiliated with Bank of Hawaii, Bank of Hawaii had to have a way to get reimbursed by Bank of New York. This may not sound like such a big deal, but remember, this was before computers were widely used. So in order to settle with one another, the merchant bank had to physically mail cratefuls of paper and sales receipts to customer banks all over the country, on an almost-daily basis. The cardholder banks then had to manually match up the sales drafts with their customer's accounts, reimburse the merchant's bank, and then finally bill the cardholders.

"It was one thing to settle accounts with five banks or even twenty-five. It was another thing to settle accounts with 150 banks, with millions of cardholders, billions of dollars in sales, and to do it without computer help, with sales drafts flying back and forth across the country every day, and with balances that didn't add up correctly half the time. Back rooms filled with unprocessed transactions, customers went unbilled, and suspense ledgers swelled like a hammered thumb." [1][2]

Bank of America had created their credit card to cut down on the operational headaches of lending money. But in an ironic twist, their decision to license the BankAmericard became an accounting nightmare of its own. As more banks signed on, the system began to break down.

NATIONAL BANKAMERICARD INC.

As licensee banks drowned in paperwork and red ink, they threatened to abandon the fledgling BankAmericard system. So in October of 1968, Bank of America summoned them to Columbus, Ohio for a meeting to sort out the technical problems with authorization and interchange. After a tense few days, Bank of America was persuaded to spin off the BankAmericard program into its own standalone entity, co-owned by all member banks. Banks would still compete for merchants and cardholders, but they agreed to cooperate at the card system level by setting operational standards and policy, developing infrastructure, sharing advertising costs, and building technology.

The newly-independent National BankAmericard Inc (“NBI”) was given a mandate by its member banks: build the behind-the-scenes apparatus that would enable banks to run their credit card operations smoothly and profitably. They quickly got to work. In 1973, NBI used computers to automate the authorization process. Three years later, they did the same to interchange. The “digitization” of these processes immediately bore fruit: transactions could now be processed 24/7/365; authorization times dropped from 5 minutes to 50 seconds; banks cleared and settled transactions overnight (instead of a week or more); and postage and labor costs were reduced by $17m ($79m today) in the first year alone.

NBI saved the program by taking a manual process—calling banks, looking up accounts, mailing sales drafts and receipts, transferring funds—and automating it. With the system finally on firm footing, National BankAmericard Inc. decided to rebrand. The name they chose was Visa.

Sources/Further Reading:

A Piece of the Action: How the Middle Class Joined the Money Class, by Joe Nocera

One from Many: VISA and the Rise of Chaordic Organization by Dee Hock

VISA: The Power of an Idea by Paul Chutkow

Financing the American Dream by Lendol Calder

Clearing and Settlement of Interbank Card Transactions: A MasterCard Tutorial for Federal Reserve Payments Analysts by Susan Herbst-Murphy

Mastercard - Value Investors Club by olivia08

Paying with Plastic: The Digital Revolution in Buying and Borrowing by David S. Evans

Payments Systems in the U.S. - Third Edition: A Guide for the Payments Professional by Carol Coye Benson

Electronic Value Exchange:Origins of the VISA Electronic Payment System by David L. Stearns

For 40 years, Costco has succeeded with a simple formula: reinvest merchandising profits into lower prices and better products; be a disciplined operator; and treat customers and employees well.

But with greater share of shopping moving online, it’s fair to wonder if the company's best days are behind it. The deck below will explore this in detail.

[Click here to download a PDF copy]

SCOTT DERUE: As you look back on your life experience, what's the most important piece of advice that you would offer everyone in the room tonight as they look forward and into their futures?

MUNGER: Well, there are a few obvious ones; they're all ancient. Ben Franklin, marriage is just like the most important decision you have and not your business career. It'll do more for you—good or bad—than anything else and Ben Franklin had the best advice ever given on marriage. He said, "Keep your eyes wide open before marriage and half shut thereafter”.

It's amazing how if you just get up every morning and keep plugging and have some discipline and keep learning, and it's amazing how it works out okay. And I don't think it's wise to have an ambition to be President of the United States or a billionaire or something like that because the odds are too much against you; much better to aim low. I did not intend to get rich. I just wanted to get independent; I just overshot.

Read More